Behavioural science

Information alone doesn't change behaviour.

Science does.

The financial sector has long relied on disclosure and information to drive customer behaviour. If people know the risks, they'll act wisely. If they understand the product, they'll engage. If they're warned about scams, they'll avoid them.

Decades of behavioural evidence — and a great deal of difficult experience — tell us this isn't how people actually work. Behaviour is shaped by context, habit, emotion, trust, social norms, and dozens of cognitive shortcuts that operate beneath conscious decision-making.

Behavioural science helps you design products, communications and services that work with how people actually think — not how we wish they did. And crucially, it gives you the outcome evidence your regulator now requires.

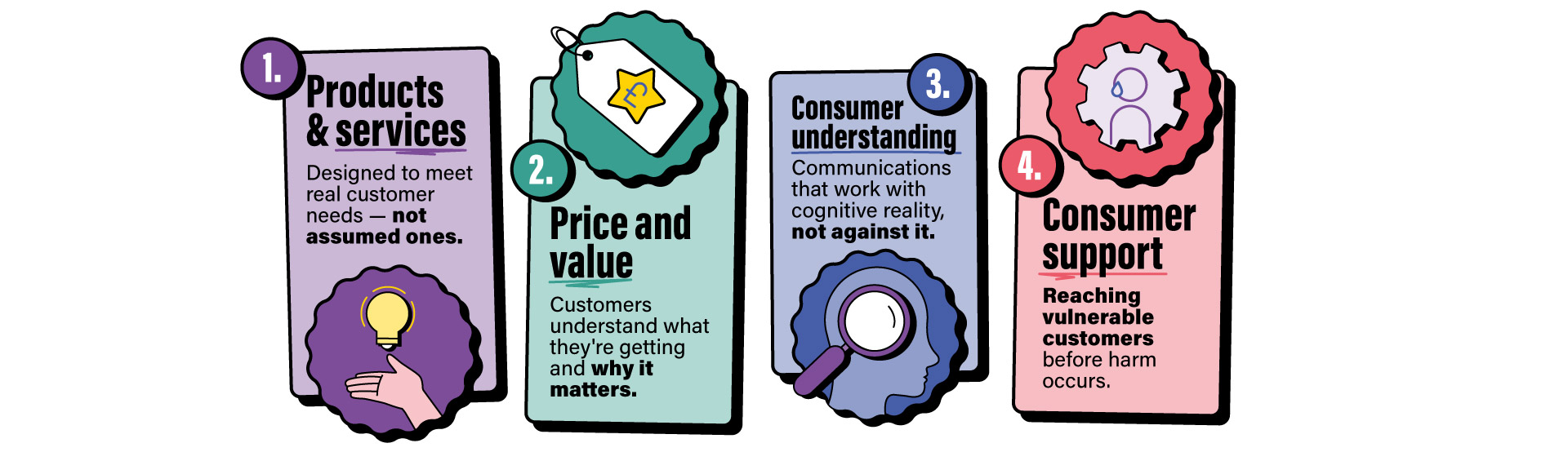

The four FCA Consumer Duty outcome areas — and where behaviour change fits

Consumer Duty requires firms to demonstrate genuine positive outcomes across four areas. Behaviour change methodology applies to all four — but is most critical where the gap between customer intention and action is widest.

Fraud & scam prevention

From awareness to behaviour change.

Fraud victims often know they should be suspicious. The problem is that scams are psychologically sophisticated — they exploit urgency, authority and trust at precisely the moments when rational decision-making breaks down. Awareness campaigns tell people what to watch for. Behavioural interventions change what they actually do when it happens.

We use COM-B analysis to identify the specific capability, motivation and opportunity barriers that leave customers exposed — then design interventions that address those barriers at the right moment, in the right context.

Vulnerable customer engagement

Reaching and supporting the customers others miss.

Customers experiencing financial difficulty, older people, people with disabilities or long-term health conditions, and those facing language barriers or digital exclusion are often the hardest to reach, and the most important to reach. Standard communications don't find them. Community-based, co-produced, behaviourally-informed approaches do.

Our approach to vulnerable customer engagement draws on deep community research, tested communication design, and trusted third-party partnerships. We don't design communications about vulnerable customers — we design them with the communities and people who experience vulnerability directly.

Financial product awareness

Removing frictions, not adding information.

Many customers don't use the products and protections available to them — not because they don't want to, but because the barriers are invisible. Default effects, friction in sign-up journeys, unclear language, and low trust all get in the way.

Removing a single unnecessary step in a sign-up journey can double take-up. Reframing a benefit as a loss avoided rather than a gain to be had shifts engagement significantly. These are not communication tweaks — they're behavioural design decisions that compound over time.

Financial resilience and debt

Beyond good advice.

Building financial resilience requires more than guidance. People in financial difficulty often know what they should do. The barriers are emotional, social and structural — shame, denial, digital exclusion, distrust of institutions, and the cognitive load of managing scarcity all prevent people from acting in their own interests.

Effective intervention means understanding those barriers through research, not assuming them, and designing responses that meet people where they are — not where it would be convenient for them to be.

Financial inclusion

Genuine community engagement.

Underserved communities face specific barriers to financial engagement: distrust of institutions built over generations, digital exclusion, language, and lived experience of financial systems that haven't worked for them. Reaching them requires genuine community understanding — not translated leaflets and extended helpline hours.

We have extensive experience co-producing engagement programmes with communities that mainstream communications routinely fail to reach. That expertise is directly applicable to the financial inclusion challenge.

Outcome evidence your regulator will accept

Outcome evidence your regulator will accept.

Consumer Duty requires firms to demonstrate that outcomes have improved — not just that processes were followed. That requires a baseline, a tested intervention, and rigorous measurement designed from the start.

We offer Social Return on Investment (SROI) analysis alongside our behaviour change programmes — helping you demonstrate the financial and social value of the work to the FCA, to your board, and to the communities you serve.

How we work:

From insight to impact — one integrated team.

Most organisations working on behaviour change buy research from one place, strategy from another, and creative from a third. The insight rarely makes it all the way through to the campaign. The campaign rarely gets evaluated against outcomes that matter to the regulator.

We're built differently. Our behavioural scientists, researchers, strategists, designers and communications specialists work as one team — carrying a single thread of evidence from the first conversation all the way through to evaluation. That's why our work produces outcomes, not just outputs.

"The use of behavioural science to inform the insights gained has been valuable. Social Change were open to adapting to the needs of the project and local requirements". [NHS Partner]

Book a call

Ready to deliver impact? Get in touch!

We'll schedule a meeting and a cuppa' (in-person or virtually) and discuss how we can make your project a reality.